ESG Pressure, Policy Push Fuel India’s Corporate Climate Revolution

India Inc’s climate playbook is no longer just about compliance – it is a strategic fusion of policy mandates and market momentum driving sustainable growth

India stands at a critical juncture, balancing rapid economic growth with environmental stewardship, aiming for net-zero emissions by 2070 as a signatory to the Paris Agreement. The key question is whether India Inc’s commitment to sustainability is driven by government mandates or market forces. In reality, it’s a dynamic interplay of both. Government mandates provide a crucial framework, while market forces act as a powerful and agile catalyst for change. Policy nudges, investor expectations, and technological innovation are converging to reshape the sustainability landscape.

The Regulatory Push: Green Mandates

India’s commitment to climate action is evident in its updated Nationally Determined Contributions (NDCs) and the ambitious Net Zero by 2070 target. To achieve these goals, the Indian government has steadily strengthened its regulatory environment. India’s regulatory framework has evolved significantly, with a slew of policies aimed at decarbonizing the economy.

Key policies include:

• Perform, Achieve and Trade (PAT) Scheme: A market-based mechanism enhancing energy efficiency in energy-intensive industries and contributing to decarbonization efforts.

• Renewable Purchase Obligations (RPOs): Mandatory rules requiring electricity distribution companies (DISCOMS) and other power procurers to buy a specific percentage of their total electricity requirements from renewable energy sources. This promotes renewable energy adoption and establishes a market for clean energy technologies.

• Energy Conservation (Amendment) Act, 2022: Empowers the government to mandate carbon trading and energy efficiency standards across sectors.

• Carbon Credit Trading Scheme (CCTS): A market-based mechanism designed to reduce greenhouse gas (GHG) emissions by incentivizing businesses to reduce their carbon footprint. It sets emission targets, allowing industries to earn and trade carbon credits for reducing emissions below their targets. Nine sectors, including Aluminum, Chlor Alkali, Cement, Fertiliser, Iron & Steel, Pulp & Paper, Petrochemicals, Petroleum refinery, and textile, are brought under this compliance mechanism, with more sectors to be included in the future.

• Extended Producer Responsibility (EPR): Holds manufacturers accountable for the lifecycle of their products, particularly in electronics and plastics.

These mandates are no longer optional, with non-compliance leading to financial penalties, reputational damage, and loss of market access. Regulations on disclosures have also been introduced. A significant development is the Business Responsibility and Sustainability Reporting (BRSR) framework by SEBI. This mandate, initially for the top 1,000 listed companies by market capitalization, has transformed corporate disclosure. It goes beyond financial reporting to encompass a comprehensive range of ESG parameters, compelling companies to measure, monitor, and publicly report their environmental and social performance. For companies like L&T, which have championed integrated reporting, BRSR reinforces their commitment to transparency and accountability. The shift from voluntary to mandatory ESG disclosure signals a clear intent from regulators to embed sustainability into corporate governance.

Beyond reporting, sectoral mandates are emerging. India’s push for 500 GW of renewable energy capacity by 2030 directly impacts industries, increasing focus on domestic manufacturing of solar panels and wind turbines, driven by schemes like the Production Linked Incentive (PLI). The National Green Hydrogen Mission is another significant mandate, aiming to position India as a leader in green hydrogen production and consumption, steering investment and innovation in hard-to-abate sectors like steel and cement.

Furthermore, the Central Consumer Protection Authority’s (CCPA) guidelines on greenwashing are a welcome step, prohibiting misleading environmental claims and requiring credible substantiation. These guidelines foster greater integrity and push companies towards genuine sustainability efforts. While sometimes perceived as compliance burdens, these mandates are vital for setting a baseline, raising awareness, and ensuring minimum accountability across industries. They act as a critical floor, preventing a race to the bottom and providing a level playing field for genuinely committed companies. For companies like L&T, operating across sectors such as construction, power, heavy engineering, and IT services, aligning with these regulations is crucial for future-proofing their business.

The Irresistible Pull of Market Forces

While mandates lay the groundwork, market forces increasingly drive India Inc.’s accelerated climate action. These forces are diverse, interconnected, and influential:

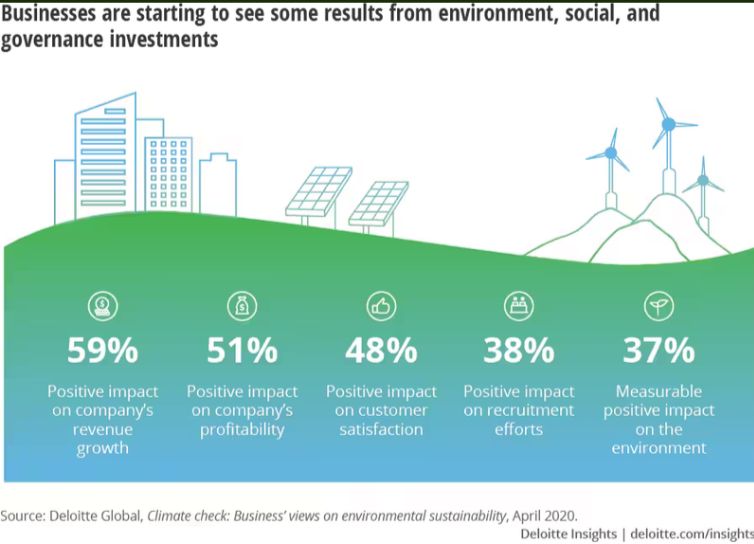

• Investor Scrutiny and Green Finance: The global financial landscape is rapidly factoring in ESG risks and opportunities. International investors, fund managers, and domestic financial institutions are integrating ESG criteria into their investment decisions. Companies with robust sustainability performance are seen as less risky, more resilient, and more attractive investments. This leads to tangible benefits: lower cost of capital for green projects, access to green bonds and sustainability-linked loans, and higher valuation for companies with strong ESG credentials. The oversubscription of India’s sovereign green bonds in early 2023 testifies to surging investor confidence in India’s green transition. Financial institutions are playing a pivotal role by reorienting lending portfolios, developing green financing schemes, and integrating climate risk assessments.

• Consumer Demand and Brand Reputation: Indian consumers are becoming more aware of environmental issues, with a growing segment, particularly younger demographics, gravitating towards brands demonstrating genuine environmental responsibility. This shift forces businesses to innovate and offer greener products and services. Companies failing to adapt risk losing market share and suffering reputational damage. The European Union’s Carbon Border Adjustment Mechanism (CBAM) is an external market force pushing Indian industries towards greater energy efficiency and decarbonization. While presenting economic challenges, it acts as a powerful catalyst, urging Indian businesses to accelerate their transition to a low-carbon economy to remain globally competitive. Increased transparency from BRSR and other disclosures ties brand reputation more closely to sustainability performance. Accusations of greenwashing can severely damage a company’s standing, making authentic climate action a non-negotiable aspect of brand building.

• Supply Chain Pressures: Many Indian companies are integral parts of global supply chains. As multinational corporations face pressure to decarbonize, they impose stringent sustainability requirements on their suppliers, including those in India. This creates a cascading effect, pushing even smaller and medium-sized enterprises (SMEs) to adopt greener practices to remain competitive within these global networks.

• Talent Attraction and Retention: The modern workforce, especially younger generations, seeks employers aligning with their values. Companies committed to sustainability and climate action are better positioned to attract and retain top talent. This is crucial in India’s competitive talent market. A progressive ESG agenda signals a forward-thinking and responsible employer.

• Innovation and Competitive Advantage: Climate action is not just about compliance or risk mitigation, but about unlocking new opportunities for innovation and competitive advantage. Investing in renewable energy, energy efficiency, circular economy models, and sustainable materials can lead to significant long-term cost savings. It also fosters the development of new products, services, and business models catering to the evolving green economy. For L&T, this translates into pioneering smart cities, sustainable infrastructure, green hydrogen solutions, and advanced water management projects. Their focus on developing technologies for client decarbonization positions them as a leader in the evolving green economy, providing a significant competitive edge. Companies proactively embracing sustainability are better equipped to navigate future disruptions and capitalize on emerging market trends.

L&T’s Journey: A Case in Point

L&T’s sustainability journey predates many current mandates. Their vision for eco-friendly growth is deeply embedded in their corporate philosophy. They aim to achieve Carbon Neutrality by 2040 and Water Neutrality by 2035, driven by foresight, strategic planning, and understanding of both regulatory expectations and market opportunities.

Their initiatives span various dimensions:

• Decarbonisation: Investing in renewable energy for their own operations (Scope 1 & 2 emissions reduction targets), improving energy efficiency across facilities, and exploring green fuels. Business units have clear targets for Scope 1 and Scope 2 emission reduction through efficiency improvements and renewable energy substitution.

• Water Stewardship: Committed to water neutrality, implementing robust water management practices, rainwater harvesting, and wastewater recycling across projects and facilities.

• Circular Economy: Increasingly adopting circularity principles in design, procurement, and construction processes, focusing on waste reduction and resource optimization.

• Green Portfolio Expansion: Actively expanding their portfolio of green offerings, including renewable energy solutions, smart infrastructure, water infrastructure, and green manufacturing capabilities, driven by high client demand. Market forces are a strong driver here, as clients increasingly demand sustainable solutions.

• Responsible Supply Chain: Working actively with their vast network of suppliers and subcontractors to enhance their sustainability performance, recognizing the importance of collective impact.

The Path Ahead: A Synergistic Future

The synergy between green mandates and market forces will only intensify. The Indian government is likely to introduce further regulations to accelerate the transition, building on frameworks like BRSR and the carbon credit trading scheme. Concurrently, global trends in sustainable finance, consumer activism, and technological innovation will continue to push companies beyond minimum compliance.

The future of corporate climate action in India will be defined by:

• Deeper Integration: Sustainability will move from a separate function to being fully integrated into core business strategy, risk management, and product development.

• Data-Driven Decisions: Emphasis on robust, verifiable data will grow, driven by reporting mandates and investor demands for transparency and accountability.

• Collaborative Action: Companies will increasingly collaborate across sectors and supply chains to address complex climate challenges that no single entity can tackle alone.

• Technological Innovation: Investments in R&D for low-carbon technologies, energy efficiency, and sustainable materials will accelerate, creating new industries and job opportunities.

• Capacity Building: A greater need for upskilling the workforce and building internal capabilities to manage and implement sustainability initiatives effectively.

India Inc. is not just responding to external pressures but genuinely embracing climate action as a strategic growth driver. Mandates provide the essential regulatory compass, but the powerful currents of market demand, financial incentives, and the pursuit of competitive advantage are truly propelling the nation’s businesses towards a sustainable and prosperous future. This dynamic interplay ensures that climate action in India is not merely a compliance exercise, but a fundamental shift towards a more resilient, responsible, and future-ready economy.

Disclaimer: The views expressed in this article are those of the author and do not necessarily reflect the views of the publication.